5 min read

Juan Andrade

How to calculate and pay Delaware Franchise Tax

Delaware Franchise Tax is a fee payable each year before March 1st for companies incorporated in Delaware. The whole process can be done in under 15 mins

For Founders

What happens if you don't file on time?

Failure to file the report and pay the required franchise taxes will result in a penalty of $200.00 plus the tax owed, both of which are subject to an additional interest charge of 1.5% per month. You could also get hit with the more expensive method of calculating so it's worth ensuring you file on time as it could cost you a lot more than $200.

How to calculate it?

There are 2 methods to calculate the tax, both are accepted by the state of Delaware. We recommend calculating using both and then using the method that results in the lower tax. Almost always for startups, that will be the Par Value Capital Method, but both are quick and simple to check.

You only need four pieces of information to do both methods:

Number of authorized shares

Number of issued shares

Par value of the shares

Gross assets of the company

Your initial number of authorized shares and the par value were set at incorporation. Unless you have authorized more (you would remember this) then check your incorporation documents for this info. Issued shares are those which have been issued to shareholders. Gross assets should be the number on your federal tax return, you can ask your accountant for this, but its usually your cash balances plus other assets like intercompany loans or machinery.

The two methods are:

Authorized Shares Method

The default method used by Delaware to calculate, and of course, the more expensive route for most. Generally, this is only really used if you have a small number of authorized shares (thousands or less). Calculate this first as it's nice and easy, and then write down that number so you can compare it to the Par Value Capital Method when you get into the filing system.

The minimum tax is $175 and it's calculated as follows:

5,000 shares or less (minimum tax) $175.00.

5,001 – 10,000 shares – $250.00,

Each additional 10,000 shares or portion thereof add $85.00

Par Value Capital Method

This is the most commonly used method by startups, most of the time it will be the cheapest.

To use this method, you need to gather some information from your financial statements. You will need to take the Total Gross Assets (most likely to be your total cash balances, but can also include any intercompany investments or loans). Find this on the Balance Sheet of your Delaware company. It should also match the Total Gross Assets reported on your Federal Tax Return (Form 1120, Schedule L). Ask your accountant if you are not sure which numbers to use.

This number is then rounded up to the nearest million.

⭐ TOP TIP: The easiest way to calculate it, is to go into the tax filer, enter your numbers and click calculate. It will tell you the tax owed.

Compare it to the Authorized Method and make sure you are using the cheaper one before you click submit. Alternatively, you can go here and download a spreadsheet-style calculator prepared by the state of Delaware.

However, if you really want to calculate it by yourself beforehand, here is the example Delaware uses to explain:

The example below is for a corporation having 1,000,000 shares of stock with a par value of $1.00 and 250,000 shares of stock with a par value of $5.00, gross assets of $1,000,000.00, and issued shares totaling 485,000.

Divide your total gross assets by your total issued shares carrying to 6 decimal places. The result is your “assumed par”.

Example: $1,000,000 assets, 485,000 issued shares = $2.061856 assumed par.

Multiply the assumed par by the number of authorized shares having a par value of less than the assumed par.

Example: $2.061856 assumed par s 1,000,000 shares = $2,061,856.

Multiply the number of authorized shares with a par value greater than the assumed par by their respective par value.

Example: 250,000 shares $5.00 par value = $1,250,000

Add the results of #2 and #3 above. The result is your assumed par value capital.

Example: $2,061,856 plus $1,250,000 = $3,311,856 assumed par value capital.

Figure your tax by dividing the assumed par value capital, rounded up to the next million if it is over $1,000,000, by 1,000,000 and then multiply by $400.00.

Example: $3,311,856 rounded up to $4,000,000. Divided by 1,000,000 = 4. 4 x $400.00 = $1,600.00

How to submit and pay

So, once you have your total assets number, which will be sometime after year-end (Dec 31st) and before the due date (March 1st), head over to the filing site here to submit and pay. This part of the process normally takes under 10 minutes to complete.

You will need your file number. If you don't know this, you can search for it here. Leave the session ID field blank and click submit.

You will then be asked to enter your Federal Employer ID, which is also known as your EIN.

Next, add your total issued shares, your total Gross Assets, and click Recalculate Tax. This will recalculate based on the Par Value Capital method - so check this is lower than the Authorized shares method you worked out previously. If it is, carry on. If not remove the gross assets and go back to the original tax number using recalculate.

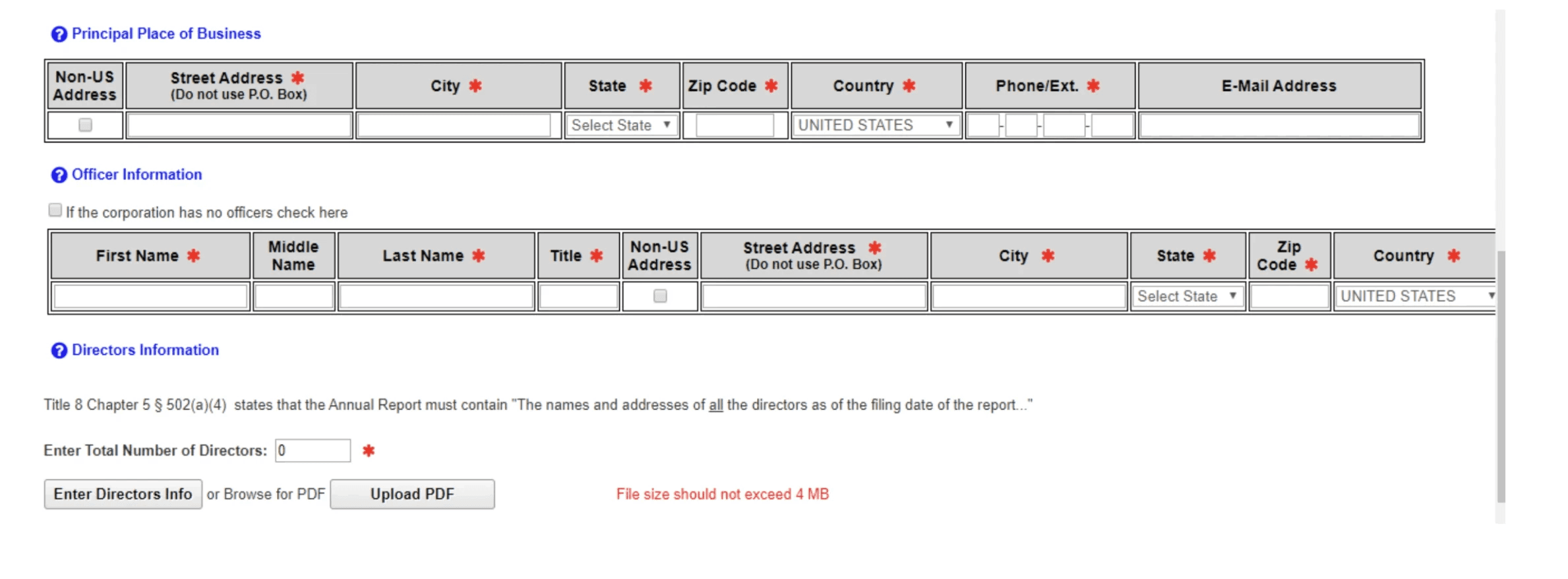

The next step is to enter the names and addresses of the company, officers, and directors. If any officers or directors don't have a US address, make sure to select the Non-US address tick box.

You need to enter the details of all registered Directors, so get this info ready beforehand.

Lastly, click "continue filing" and grab a credit card to pay the fee.

Job done.

Know someone who needs to read this?

Juan Andrade

Founder, Caribou

Further reading

Our team has worked in the industry for years, and we’re here to share what we have learnt with you.